Based on the previous year’s operations, corporate tax filing in Singapore is tricky. Although the tax basis is the same in many other countries across the globe, the tax rate for the income of local and foreign firms in Singapore is just 17%. On top of that, the country offers a tax exemption plan for new ventures, except for those:

- Whose primary pursuit is investment holding; and

- Engaged in developing estate for investment, sale, or both.

To qualify for the tax exemption plan, the new firm must meet these requisites:

- Setup in Singapore;

- Singaporean tax resident for the taxable year; and,

- Have its share capital be held openly by only 20 shareholders during the taxable period where all are individual shareholders. If not, at least a shareholder exists as a person owning 10% or more of the business’ ordinary shares.

Who is Required to Perform Corporate Tax Filing in Singapore?

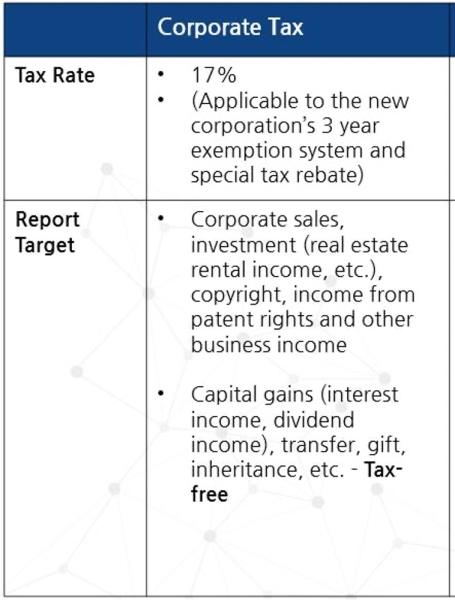

No matter the firm’s tax-residency status, it is obligated to pay Singapore’s corporate tax as stated in the Income Tax Act. This tax is based on any taxable income gained by doing business in Singapore, plus foreign income sent into the country.

Note that Singapore tax-resident firms enjoy several welfares compared to non-tax resident firms. So, for tax purposes, what constitutes a Singapore company? Here’s an itemized description:

- The business entity is listed under the law in Singapore, in particular, the Companies Act 1967;

- A company’s name usually includes “Ltd” or “Pte Ltd”;

- The foreign company is registered in Singapore, including a foreign firm’s branch.

Note that a partnership or sole proprietorship business does not do corporate filing in Singapore. Finally, a company is deemed a tax resident of Singapore when its management and control are carried out in the country. Thus, the firm’s board meetings take place in Singapore when making decisions on important matters. In addition, these companies enjoy the reliefs from the Double Taxation Agreements that Singapore holds with treaty countries.

Corporate Tax Filing in Singapore: What Every Foreign and Local Company Need to Know

As you can see in the tables below, the tax rate is 17%, which applies to new corporations’ 3-year exemption system and special tax rebates. Note that the tax exemption for startups fosters entrepreneurship and does not apply to certain companies.

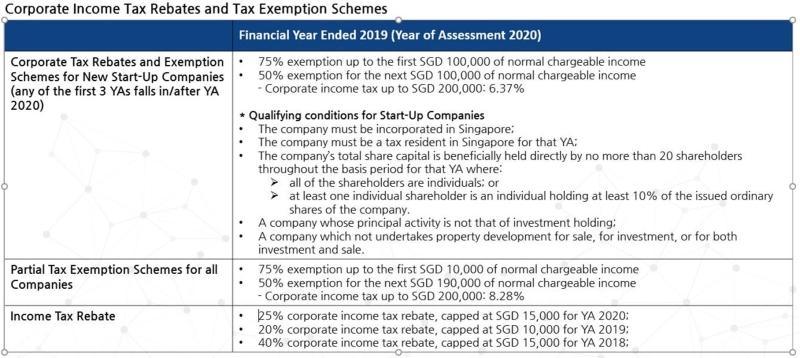

On the other hand, existing businesses, such as investment holding firms and those undertaking property development, may avail themselves of the partial tax exemption. Under the Start-up Tax Exemption Scheme of the 2018 Budget of Singapore, the exemptions are:

• 75% on the initial SGD 100,000 of the normal chargeable income

• 50% on the following SGD 100,000 of the normal chargeable income

This exemption scheme applies to qualifying companies only for their first 3 consecutive YAs. From the fourth YA onwards, companies can enjoy partial tax exemption. Learn how to determine the first 3 YAs of your company.

The table above also includes the Partial Tax Exemption scheme, the due date for submitting the Income Tax Return or ITR with its attachments, which is November of each calendar year, and the forms to use.

The ITR is different from the ECI since this is just an estimated figure of what the company expects to earn. Per tax law, all companies must file their ITR, even when there is no income during the taxable year unless IRAS has granted waiver to file income tax return.

Corporate Tax Filing in Singapore: Filing and Payment Process

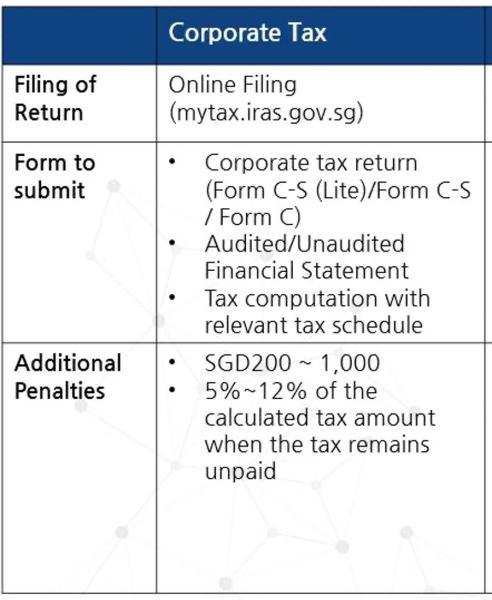

Effective April 11, 2021, companies in Singapore are obligated to use the government digital facilities for businesses, known as G2B, using Singpass. Thus, all filing is via mytax.iras.gov.sg.

File the ECI or Estimated Chargeable Income form, unless exempted

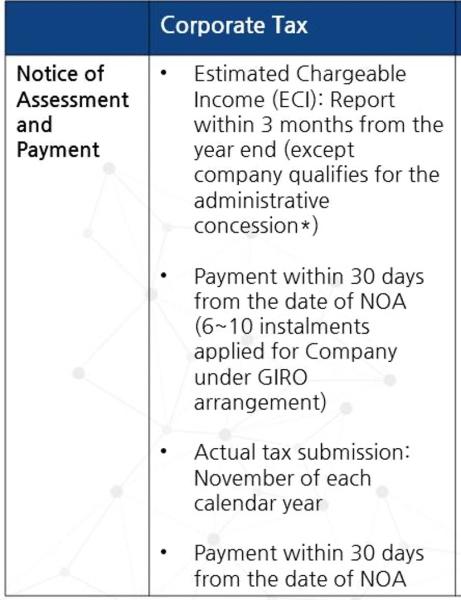

The filing and payment process for corporate taxes in Singapore generally starts by filing this form. First, the company provides the Inland Revenue Authority of Singapore with an estimated figure of its taxable income within a quarter of its financial year.

All companies must file ECI within three months from their financial year-end. The exception is when the company meets the requirements for the waiver on ECI filing. For example, if the firm’s fiscal year-end is March 31, 2021, then the deadline to file the ECI is June 30, 2021, for the 2022 Year of Assessment.

Receive IRAS’ NOA or Notice of Assessment

After filing, IRAS will check the forms to facilitate their issuance of an NOA. The NOA provides a detailed report of the tax liabilities of the company. It also gives the company a chance to object to the tax assessment of IRAS if it wants to.

Pay the Assessed Corporate Tax

All companies need to settle the tax amount within 30 days from the date of receipt of the NOA unless qualified to pay by installment. Payment can be through various methods, such as internet banking, interbank GIRO, telegraphic transfer, or cheque.

Corporate Tax Filing in Singapore: Penalties for Non-Compliance

Non-Payment or Late Payment

Failure to settle the levied corporate tax as scheduled may result in a five percent penalty. On top of that, a one percent penalty compounds for every month the assessed tax remains outstanding. In some instances, IRAS may likewise take further legal or enforcement actions to collect the overdue tax.

Tax Evasion

Tax evasion occurs when a taxpayer deliberately gives IRAS false or partial information to bring down their tax liability and obtain the wrong refund or tax credits. Note that Singapore regards tax evasion as a severe illegal offense. Thus, IRAS observes a sophisticated program to investigate cases of alleged tax evasion. This may consist of surprise visits or searches of home and company premises to find accounting records and relevant documents, in addition to obtaining or checking for information from banks and other financial institutions.

Investigations of this kind may last from 15 months to two years. When proven that the ITR is incorrect so as to evade taxes, IRAS may impose any or a mix of the following:

- Financial punishments of 400% at the maximum of the undercharged tax;

- Fines of SGD 50,000 or below; or

- Five years imprisonment or less.

Tax Filed Incorrectly

Where the ITR is filed incorrectly without the intention to avoid taxes, IRAS may impose any or a mix of the following:

- Financial penalties to a maximum of 200% of undercharged tax;

- Fines not exceeding SGD 5,000; or

- Three years or less of imprisonment.

Commonly Faced Issues and Expert Tips for Efficient Corporate Tax Filing in Singapore

Accurate and timely corporate tax filing in Singapore is essential to maintaining compliance with the Inland Revenue Authority of Singapore (IRAS) and ensuring smooth business operations. However, many companies, especially newly incorporated ones, encounter challenges that can lead to errors, delays, or unnecessary penalties. Understanding these common pitfalls and applying practical strategies can help businesses streamline their filing process and avoid compliance risks.

Inaccurate or Incomplete Tax Information

One of the most frequent mistakes is submitting inaccurate or incomplete information in the tax return. Companies can easily overlook income adjustments, double-count certain deductions, or fail to reconcile accounting profits with taxable income. Another common issue is the misuse of depreciation instead of capital allowances when claiming deductions for fixed assets. Since IRAS specifically requires capital allowance claims, not adhering to these rules can result in disallowed claims and higher tax liabilities. In addition, businesses sometimes neglect to maintain proper accounting records for the required five-year period, which can lead to compliance issues during audits or verification requests.

Missed Filing Deadlines

Late submission of tax returns remains another major concern. Companies must file their Form C-S, C-S (Lite), or Form C by the statutory deadline of 30 November each year. Missing this deadline can trigger late filing penalties, enforcement actions, and potential reputational risks. Similarly, failing to submit the Estimated Chargeable Income (ECI) within three months of the financial year end can also lead to unnecessary complications.

Enhancing Filing Efficiency

To ensure efficient corporate tax filing in Singapore, companies should establish an internal review process well before the filing deadline. Preparing tax computations and supporting schedules in advance allows time to identify discrepancies and correct errors. Businesses should also ensure that their authorized personnel are granted the appropriate CorpPass access for tax filing to prevent last-minute administrative delays. Lastly, keeping up-to-date with IRAS announcements and filing guidelines helps ensure that companies remain compliant with the latest requirements and avoid costly oversights.

By adopting these proactive measures, companies can enhance accuracy, reduce compliance risks, and ensure a smoother corporate tax filing experience in Singapore.

To Conclude

Considering the severe penalties, it stands highly recommended that all companies should enlist the services of an expert tax firm. Companies can then ensure their corporate tax filing in Singapore and payments are timely and accurately prepared. Check out PREMIA TNC for corporate tax services.