In today’s interconnected global economy, maximizing returns from diverse income sources is essential, especially when it comes to Taiwan-sourced income. This article serves as your comprehensive guide to unlocking the full potential of your investments in Taiwan. We will look into expert strategies and solutions tailored to help you optimize returns while navigating the dynamic nuances of the Taiwanese market.

Whether you are a seasoned investor or just exploring opportunities in Taiwan, our insights are designed to assist you in making informed decisions, adopting a cautious approach in line with the local tax landscape. Get ready to embark on a path that leads to not only maximizing returns from your Taiwan-sourced income but also effectively managing tax risks for sustained financial success.

Background of Taiwan-Sourced Income

The tax office in Taiwan has gained a reputation for asserting that nearly all payments made by Taiwanese entities for services acquired from overseas profit-seeking enterprises should be considered Taiwan-sourced income, with only a few clearly defined exceptions. The country’s court system typically supports the tax office’s stance, leading to the taxation of many foreign profit-seeking enterprises in Taiwan for fees earned from services conducted outside of Taiwan. Acknowledging the controversy surrounding the “source of income,” the Ministry of Finance in Taiwan issued a ruling on September 3, 2009, with the aim of providing better regulation on this matter.

The Determination Principles of Taiwan-Sourced Income

On September 3, 2009, the Ministry of Finance instituted the ‘Income Tax Act Article 8 Principles for Determining Taiwan-sourced Income.’ Over time, this definition of Taiwan-sourced income has evolved through interpretative orders that lean towards taxpayer favorability. The criteria for determining Taiwan-sourced income encompass various categories:

1. Service remuneration

Income is ascertained based on the location of service provision. Remuneration for services rendered exclusively outside Taiwan by foreign profit-making enterprises is not deemed to be Taiwan-sourced income. If services involve both domestic and international elements or require participation from entities within Taiwan, the income is considered Taiwan-sourced unless a clear distinction can be made.

2. Interest

Income from interest earned by Taiwan’s government, domestic legal entities, and residents.

3. Rent

Income generated from registered and recorded movable or immovable property within Taiwan.

4. Royalties

Any income derived from patents, trademarks, copyrights, secret methods, and various patent rights utilized in Taiwan. Payments by domestic profit-making enterprises for the authorization of intangible assets utilized abroad due to outsourcing, manufacturing, or research are considered Taiwan-sourced income.

5. Property transaction income

Income from registered and recorded movable or immovable property within Taiwan.

6. Operating business profits

Business profits are distributed based on the contribution level within and outside Taiwan.

7. Prizes from competitions

Prizes are deemed Taiwan-sourced income if the event takes place in Taiwan and is awarded by individuals within the country.

8. Other incomes

Comprehensive principles for determining income when it cannot be clearly attributed to the first eight categories.

Following the implementation of these principles, companies should conduct a thorough review of existing contracts to ensure optimal tax planning. This includes considerations for the nature of services, differentiation between domestic and foreign services, and contractual agreements covering ownership rights and obligations.

Where Premia TNC comes into the picture

At Premia TNC, we specialize in navigating the intricacies of Taiwan-sourced income, offering tailored services to meet your unique needs. Here’s how we can assist you in this specific area:

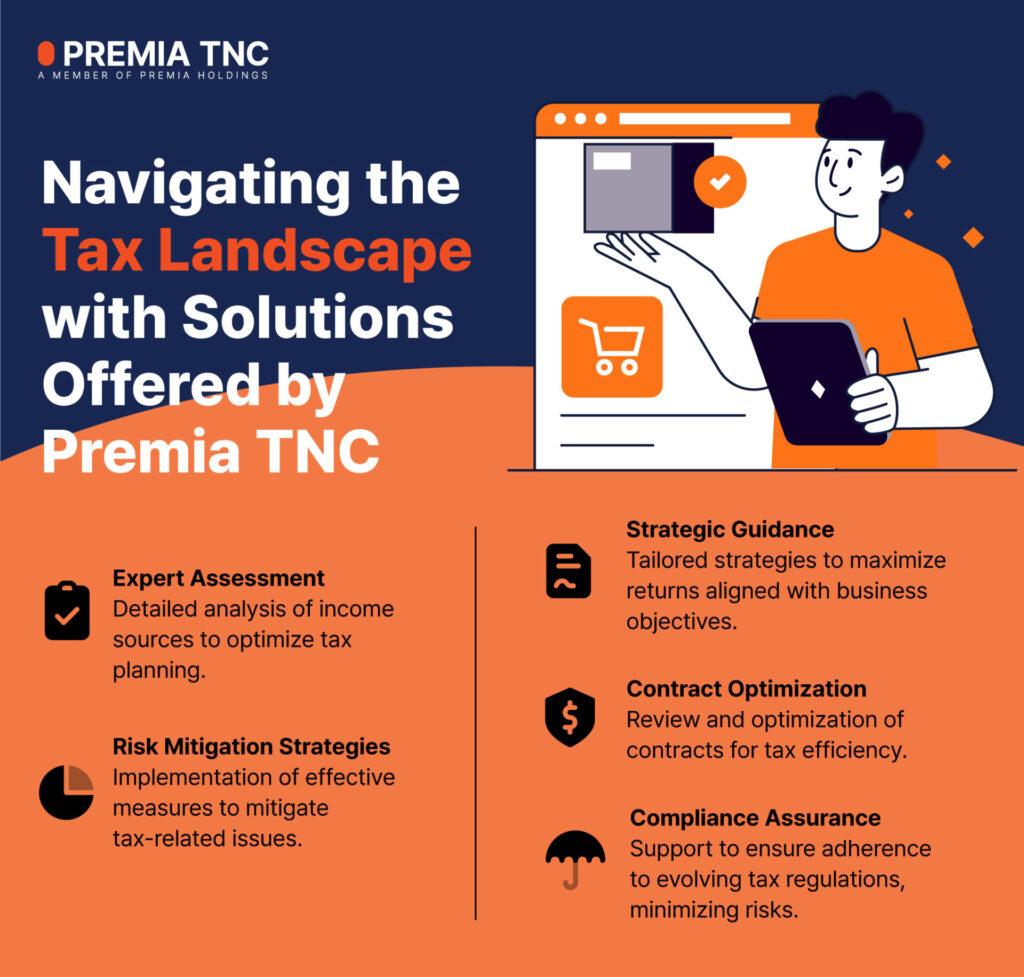

Expert assessment:

Our team is well-versed in the complexities of Taiwan-sourced income. We conduct expert assessments, meticulously analyzing income from various sources, including service remuneration, interest, rent, royalties, property transactions, operating business profits, prizes from competitions, and other categories outlined by the Ministry of Finance.

Strategic guidance:

Understanding the nuances of Taiwan’s tax landscape is crucial. We provide strategic guidance on optimizing your Taiwan-sourced income, ensuring that you benefit from expert insights to make informed decisions aligned with your business objectives.

Compliance assurance:

Staying compliant with evolving tax regulations is challenging. Premia TNC offers dedicated support to ensure that your business operations adhere to the latest legal requirements, minimizing the risk of penalties and ensuring seamless operations.

Risk mitigation strategies:

With stringent penalties for withholding obligation violations, adopting a cautious approach is paramount. Our team assists you in implementing effective risk mitigation strategies, minimizing the potential for tax-related issues in the context of Taiwan-sourced income.

Contract optimization:

We review and optimize your existing contracts to align with the latest taxation principles, focusing on service nature, differentiation between domestic and foreign services, and ownership rights and obligations. This ensures that your contractual agreements are optimized for tax efficiency.

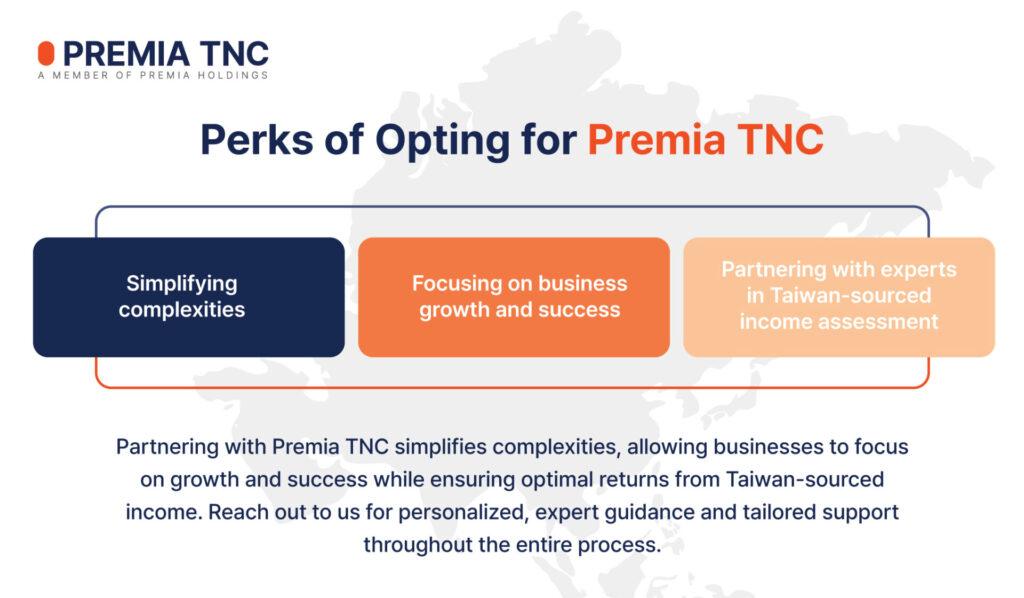

Choosing Premia TNC means partnering with a team committed to delivering excellence in Taiwan-sourced income assessment. Let us simplify the complexities, allowing you to focus on the growth and success of your business.

FAQs

Q1: What is considered Taiwan-sourced income?

A1: Taiwan-sourced income includes earnings derived from various sources, such as service remuneration, interest, rent, royalties, property transactions, operating business profits, prizes from competitions, and other categories outlined by the Ministry of Finance.

Q2: How is service remuneration taxed in Taiwan?

A2: Service remuneration is taxed based on the location of service provision. If services are provided solely outside Taiwan by foreign profit-making enterprises, the income is not considered Taiwan-sourced. However, for services provided both within and outside Taiwan or involving domestic participation, the income is deemed Taiwan-sourced unless clearly distinguished.

Q3. Are there specific criteria for determining Taiwan-sourced income from property transactions?

A3. Yes, income from property transactions is considered Taiwan-sourced if the registered and recorded movable or immovable property is located within Taiwan.

Q4. How are royalties taxed in Taiwan?

A4. Royalties, including those for patents, trademarks, copyrights, and various patent rights used in Taiwan, are considered Taiwan-sourced income. Payments made by domestic profit-making enterprises for authorized intangible assets used abroad are also subject to taxation.

Q5. What risk management strategies can businesses employ to mitigate Taiwan-sourced income-related issues?

A5. Businesses can adopt a cautious approach, withholding taxes when making payments to foreign enterprises for non-international trade-related amounts. Thoroughly reviewing contracts, ensuring compliance with evolving tax regulations, and seeking expert advice for risk mitigation are recommended strategies.