In the dynamic world of business, statutory compliance represents a crucial cornerstone, ensuring companies operate within the legal frameworks established by governing bodies. This comprehensive exploration delves into the essence of statutory compliance, highlighting its importance in maintaining the legal and financial health of businesses. By understanding and adhering to various statutory requirements, companies can navigate the complexities of the business environment more effectively, fostering sustainability and growth.

The Importance of Statutory Forms and a Company’s Constitution

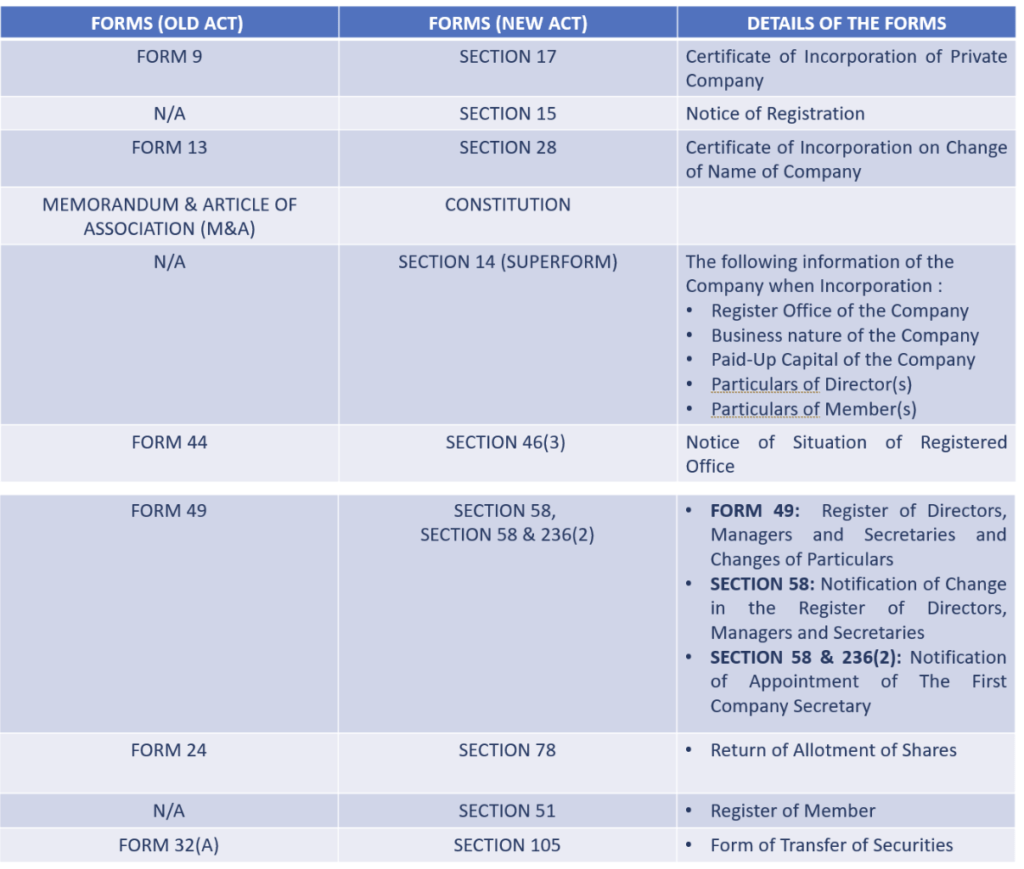

Statutory forms and a company’s constitution are fundamental to establishing and maintaining a business’s legal status. These documents, which include incorporation certificates and changes of name certificates, lay the groundwork for a company’s identity, operational guidelines, and governance structures. Transitioning from old legislative frameworks to new ones requires a meticulous understanding of these forms, ensuring businesses remain compliant with current laws and regulations.

Company’s Constitution Vs Memorandum Of Association (M&A)

Historically, the M&A were two separate documents that collectively formed the constitution of a company under the Companies Act 1965 and earlier legislation.

Memorandum of Association

This legal framework is central to Malaysia’s strategy to prevent ML and TF, ensuring that financial entities operate with integrity and within the bounds of the law. This document outlined the company’s fundamental conditions upon which it was granted incorporation. It included the company’s name, whether its liability is limited by shares or by guarantee, and what it aims to do (objects clause), including the scope and limits of its operations. It effectively served as the company’s charter.

Constitution

With the advent of the Companies Act 2016, the concept of a single unified document known as the Constitution came into effect, replacing the need for separate Memorandum and Articles of Association for new companies.

Constitution: Under the new act, companies are no longer required to have a separate Memorandum and Articles of Association. Instead, they may choose to adopt a single document called a Constitution after incorporation. This Constitution includes both the fundamental conditions of the company’s operation (similar to the Memorandum) and the internal governance rules (like the Articles). If a company does not adopt a separate Constitution, then the default provisions in the Companies Act 2016 will apply to that company.

Not Compulsory

Unlike the Memorandum and Articles of Association under the old legislation, it is not compulsory for a company to adopt a Constitution unless it is a company limited by guarantee. However, having a Constitution allows a company to customize its governance rules to suit its specific needs better, which can be advantageous.

In summary, while the Memorandum and Articles of Association were previously two mandatory documents required for the formation and governance of a company, the modern Constitution serves as an optional, singular, comprehensive document that governs a company’s operations and internal management under the current Companies Act 2016. The Constitution provides flexibility for companies to adopt bespoke governance rules that are not covered by the Act’s default provisions.

Annual Submission

Under the Companies Act 2016, all registered and existing companies must lodge annual submissions which comprise of:

1. Annual Return

Annual Return comprise all company’s information such as the business activities, the location of the business, registered office, particulars of its director(s), companies’ secretary(ies), and members with its shareholding particulars in the company. All these particulars are to be submitted yearly within thirty (30) days of the incorporation anniversary date of the Company.

2. Financial Statements and Reports

A company’s financial statements and reports contain significant information that stakeholders can use to estimate the company’s earnings potential and financial health.

The financial year end of financial statements and reports need to be fixed within eighteen (18) months from the date of its incorporation and subsequently, within six (6) months of its financial year end (the deadline).

The financial statements and reports must be circulated to all shareholders (s) within six (6) months of its financial year-end. Thereafter, lodge the audited financial statement to SSM within thirty (30) days from the circulation date.

EPF/SOCSO/PAYROLL/CP22/FORM C/ CP204/EA FORM

Employees’ Provident Fund (EPF)

Employees’ Provident Fund (known as EPF, or KWSP in Malay) is a Malaysian government agency that manages a compulsory savings plan and retirement planning for private and non-pensionable public sector employees.

The EPF functions through monthly contributions from employees and their employers towards saving accounts. While in savings these funds may be used in various investments by the EPF or, in some cases, by the members themselves.

The employer is required to register and make payments for their employees’ contributions at the specified rate on or before the 15th of the subsequent wage month. The employer must initially remit both their and the employee’s shares to the EPF.

Social Security Organisation (SOCSO)

Employers are also obligated to deduct contributions for the Social Security Organisation (SOCSO) and Employment Insurance System (EIS) on behalf of employees. Additionally, employers are required to make a small contribution to employees’ accounts from their own funds.

SOCSO and EIS are different contributions, but they are under the same organisation, PERKESO.

Employers can refer to the table published by PERKESO on the official website for the SOCSO rate. The rate for EIS is 0.2% of employees’ wages, contributed by both employees and employers.

The deadline for contributions is the 15th of the subsequent month.

Payroll

Payroll refers to the compensation that businesses must pay their employees at a set time and on a fixed date.

The payroll process can include tracking hours worked for employees, calculating pay, and distributing payments via direct deposit or cheque.

Companies must also maintain accounting records and set aside money for Medicare, Social Security, and unemployment taxes.

CP22

Notifications of New Employee

- The employer is responsible for reporting new employees who are or are likely to be chargeable to tax within 30 days from the date of commencement of employment using Prescribed Form CP22 (Notification Form By Employer For New Employee).

- Form CP22 can be submitted to the Inland Revenue Board Malaysia (IRBM) office that handles the Employer tax (E number) file or to the nearest IRBM office.

- The completed Form CP22 must contain particulars of the employer, particulars of the new employee, particulars of monthly remuneration, and duly signed declaration.

Income Tax Return for Company (FORM C)

The Corporate Income Tax is submitted using Form C to IRBM. All payments will be through the online portal (cash and cheque payment is not allowed).

The deadline for the submission of Form C should be within 7 months after the close of the accounting period.

E-Filing (online filing submission) can be submitted within 8 months from the date after the close of the accounting period.

CP204

The CP204 form is prescribed under the Income Tax Act 1967 and serves as a tax instalment payment schedule. It is used by businesses, including newly incorporated companies, to report their estimated tax payable in instalments throughout the basis period.

Company in operation

Companies, cooperatives, trust bodies, and LLPs in operation must submit e-CP204 not later than 30 days before the commencement of the basis period for a year of assessment.

New companies operating

For companies, cooperatives, trust bodies, and LLPs that have just commenced operations and have a first basis period for a year of assessment of not less than six (6) months, e-CP204 must be submitted in a period of three (3) months from the date of commencement of operations of companies, cooperatives, trust bodies, and LLPs.

EA FORM

EA Form officially known as the “Statement of Remuneration from Employment”, put simply Form EA is a summary of the employee’s earnings from the employer for the year.

The purpose of Form EA is to enable employees to file their taxes properly and declare their earnings to IRBM. That way, it can be determined which tax bracket they fall under.

The employer is required to generate Form EA for each employee, regardless of their full-time, part-time, or fixed-term status, as long as they have worked for more than seven days and received payment for their services. This form must be prepared and provided to the employees by no later than 28 February each year. However, it is not required to be submitted to the tax authorities.

Conclusion

In summary, the realm of statutory compliance is a fundamental aspect of maintaining a business’s legal and operational integrity. The transition from traditional Memorandum and Articles of Association to a more flexible Constitution under the Companies Act 2016 offers companies the ability to customize their governance structures. Staying on top of annual submissions, employee welfare contributions such as EPF and SOCSO, and accurate tax filings including CP22, Form C, CP204, and EA Form is paramount. These efforts not only ensure legal adherence but also reinforce a company’s reputation and contribute to its long-term stability and success. As the corporate world evolves, the mastery of these compliance nuances becomes a strategic advantage for any business.